The Vietnamese stock market is witnessing a highly contradictory transition period. Recently, the VN-Index has continually conquered new milestones, establishing a historic peak in mid-May 2026; simultaneously, FTSE Russell officially confirmed the roadmap to upgrade Vietnam to a Secondary Emerging Market, effective from 21/09/2026. Contrary to expectations of welcoming large-scale international capital inflows, the market has instead experienced a record-breaking net withdrawal wave by foreign investors. This sharp contrast between market movement and the capital outflow of foreign investors reflects technical bottlenecks, shifts in global financial interest, along with inherent macroeconomic risks that investors need to monitor.

Source: FiinPro, PHFM Compiled

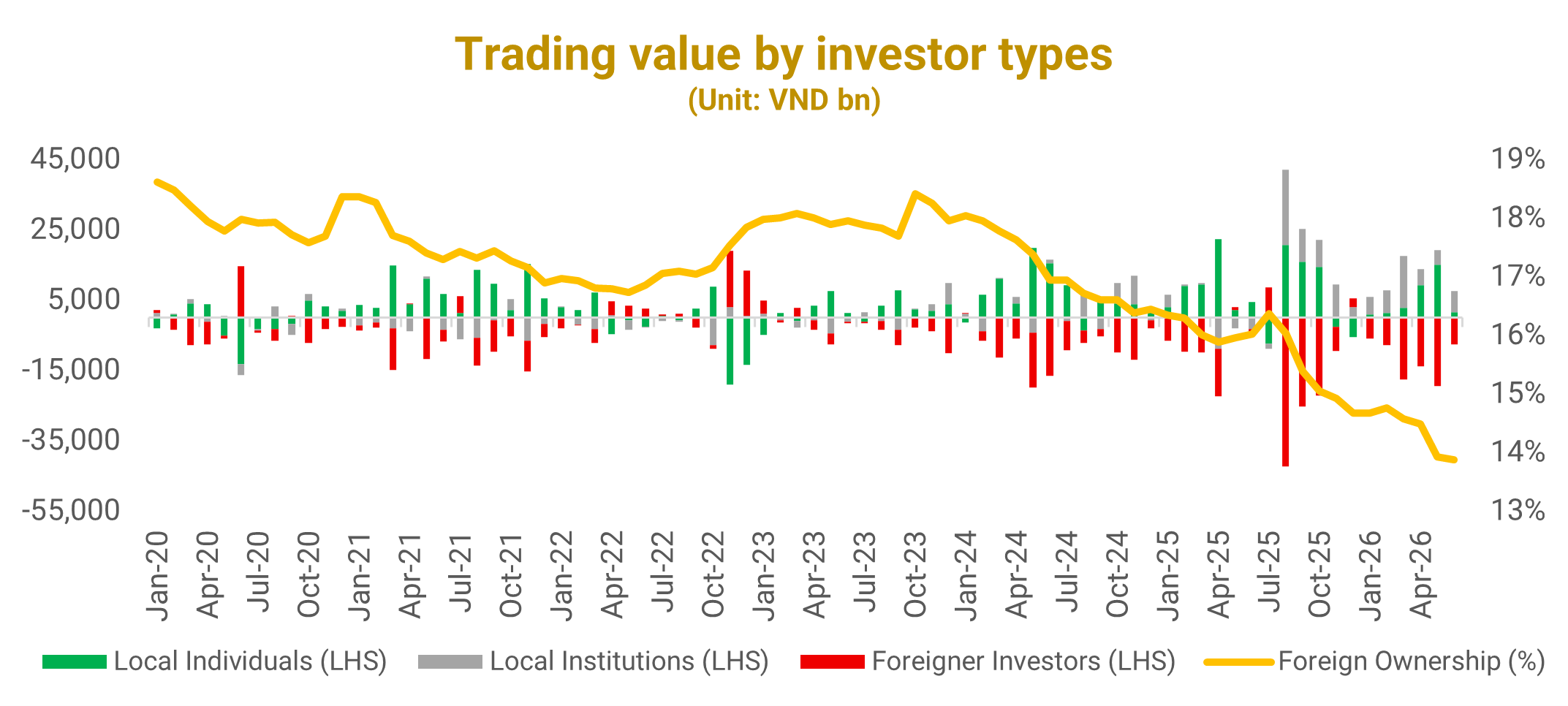

The foreign capital outflow of the Vietnamese stock market became distinct from the beginning of 2023. Cumulative from 2023 to May 2026, foreign investors have net withdrawn nearly USD 11.8 billion. The foreign ownership limit (FOL) ratio calculated by market capitalization on the HoSE floor has dropped from 17.98% (2023) to a mere 13.88% (mid-2026). So why has a market filled with potential like Vietnam recorded such strong capital flight?

1. Prolonged Negative Interest Rate Differential

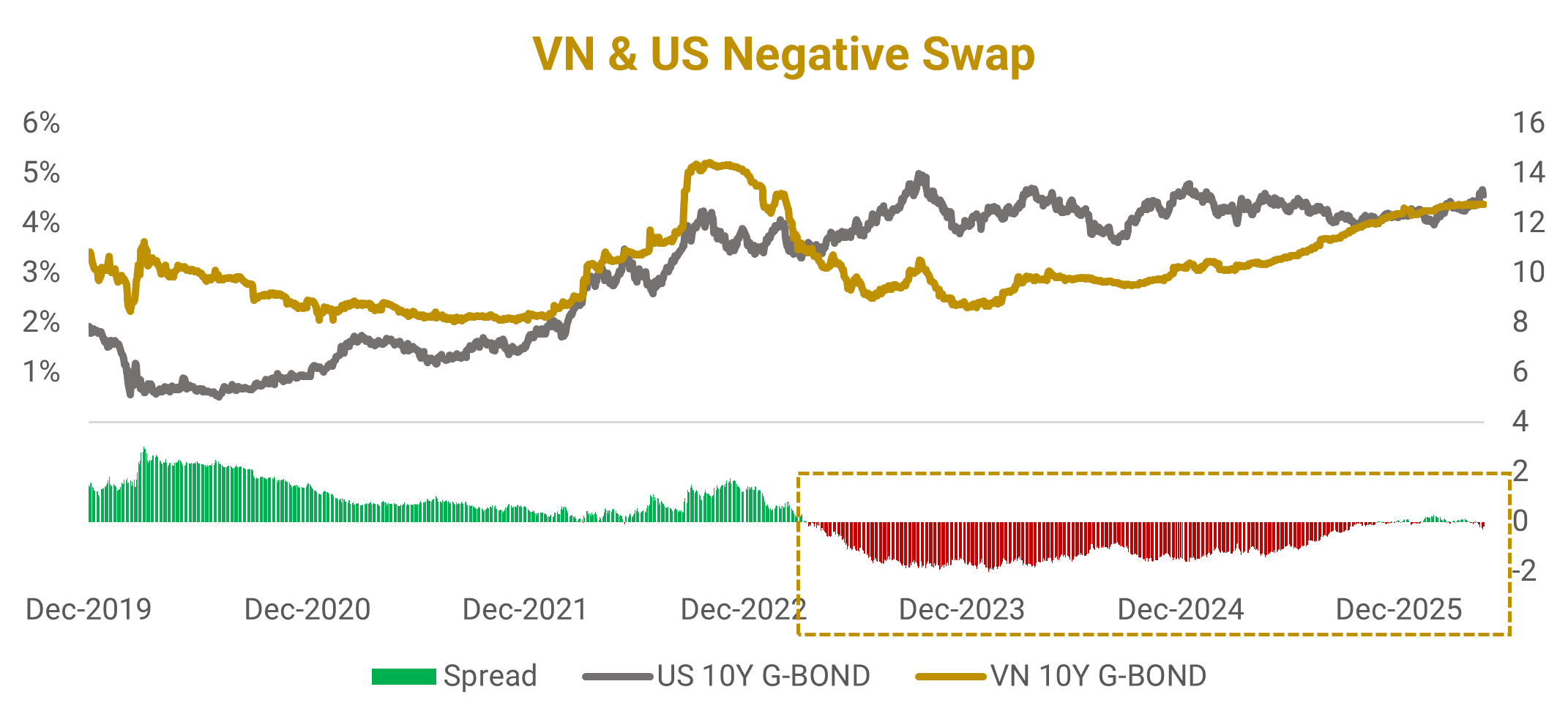

From 2023, while the US Federal Reserve (FED) continually raised interest rates to curb inflation, the State Bank of Vietnam (SBV) proactively moved in the opposite direction of policy by lowering policy rates to support the economy. This policy divergence immediately created a negative interest rate differential (negative swap) between VND and USD, pushing the exchange rate into tension and driving foreign investors to take a defensive stance by withdrawing capital.

Source: Investing.com, PHFM Compiled

Although the interest rate differential has narrowed as Vietnam ended its monetary easing cycle and reversed to raising interest rates, exchange rate pressures remained.

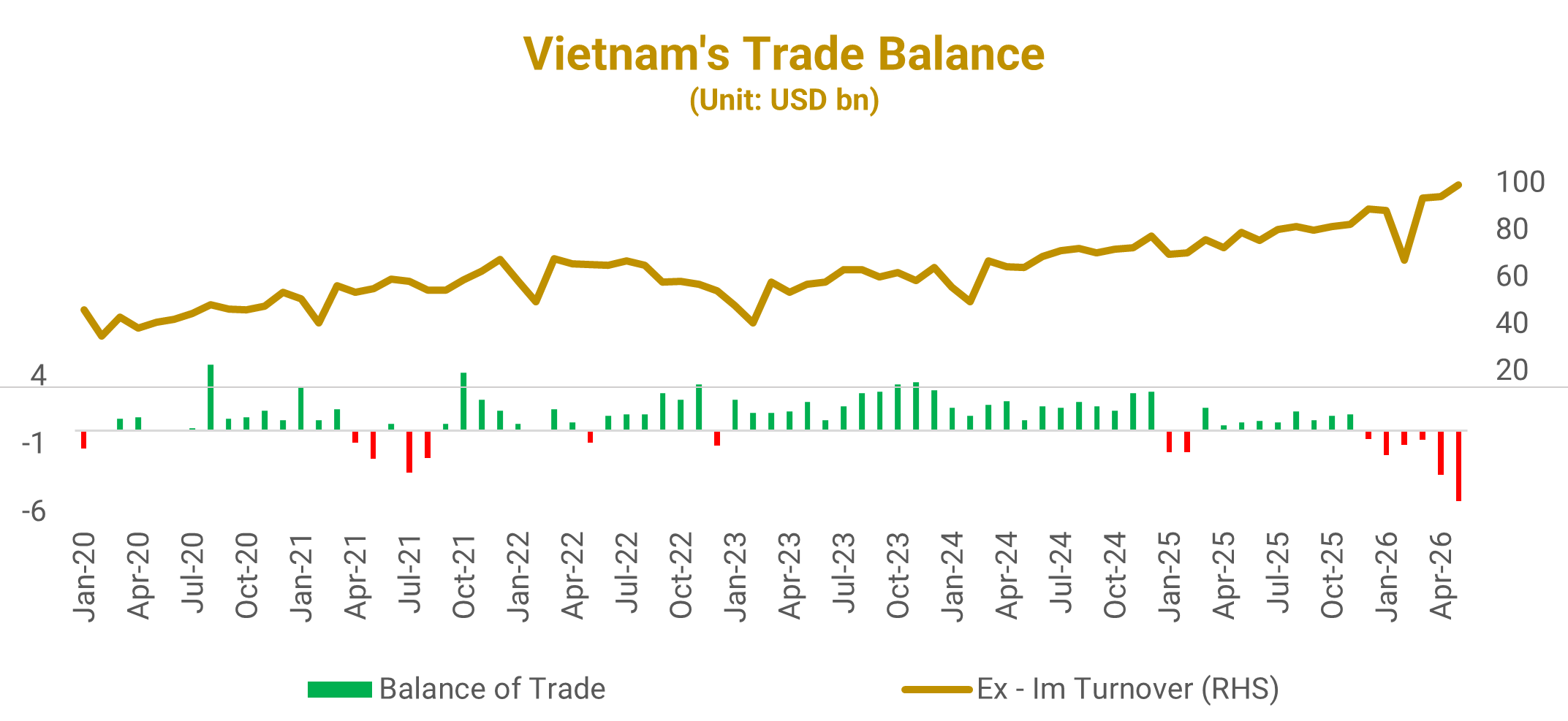

In the first five months of 2026, Vietnam fell into a record trade deficit of up to USD 13.8 billion, a stark contrast to the trade surplus of USD 5.1 billion in the same period last year. This severe decline was due to corporates aggressively increasing the import of energy and raw materials to preempt risks of supply chain disruptions. Although this serves as preparation for the year-end export cycle, the large trade deficit still exerts major pressure on the USD/VND exchange rate.

Source: NSO, PHFM Compiled

Concurrently, inflationary pressures are rising as the May CPI exceeded the 5% threshold driven by escalating energy prices, pulling the average CPI for the first five months up by 4.31%. High inflation combined with tightened liquidity has driven interbank interest rates up sharply. Exchange rate risks and rising capital costs have eroded investment performance converted back into USD, prompting foreign investors to opt for safety by taking profits and withdrawing capital.

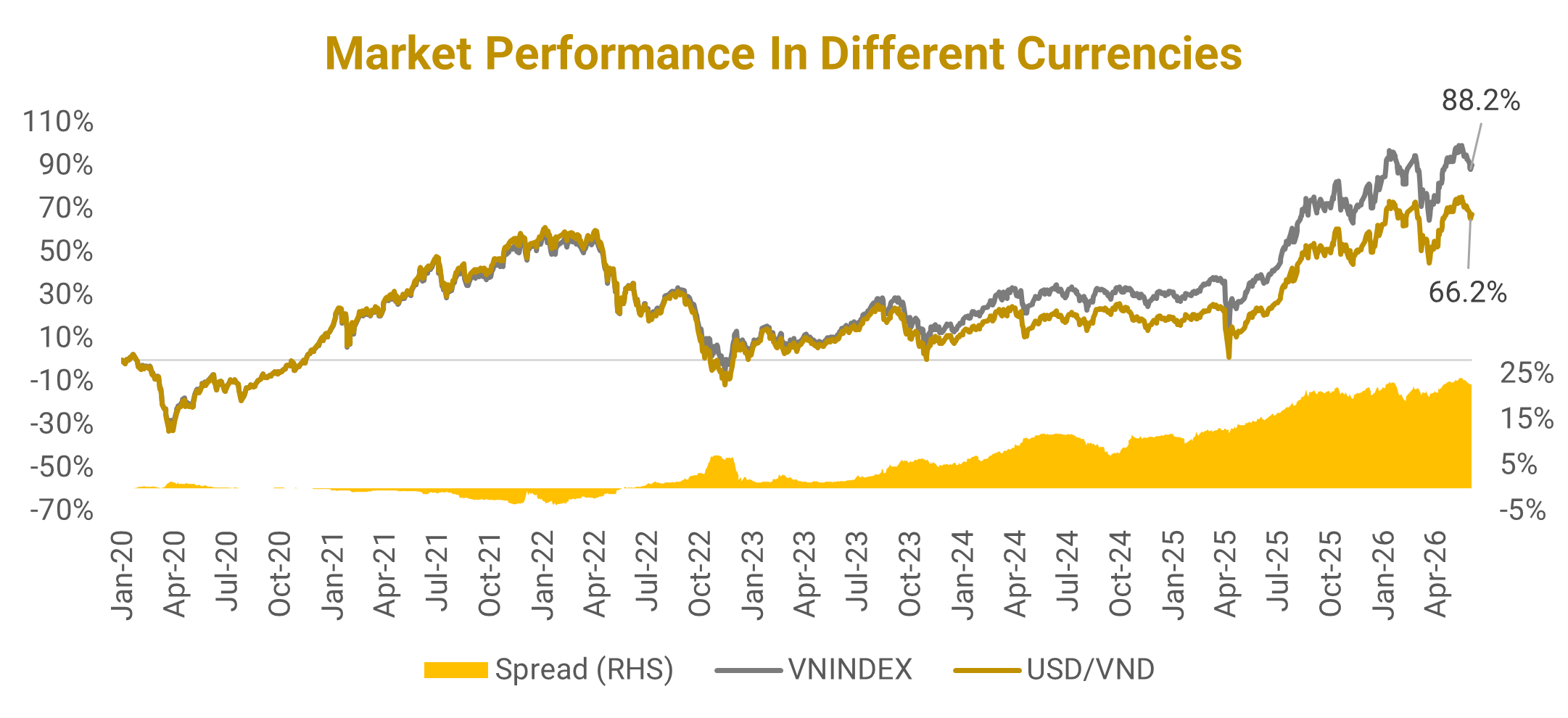

To visualize the impact of the exchange rate, suppose an international investor deployed capital into the Vietnamese stock market in 2020 and applied a buy-and-hold strategy:

– In term of VND, investors are getting a cumulative return of approximately 90%.

– However, since foreign cash flows must ultimately be converted back to the base currency upon liquidating positions, the sharp depreciation of the VND over the past four years has directly eroded 22% of that nominal performance. This decline does not stem from stock-picking capabilities or a decay in corporate fundamentals, but is purely the opportunity cost of holding a weaker currency during a volatile macroeconomic cycle.

Source: FiinPro, PHFM Compiled

2. Structural Industry Mismatch and The Lack of Technology Pillar

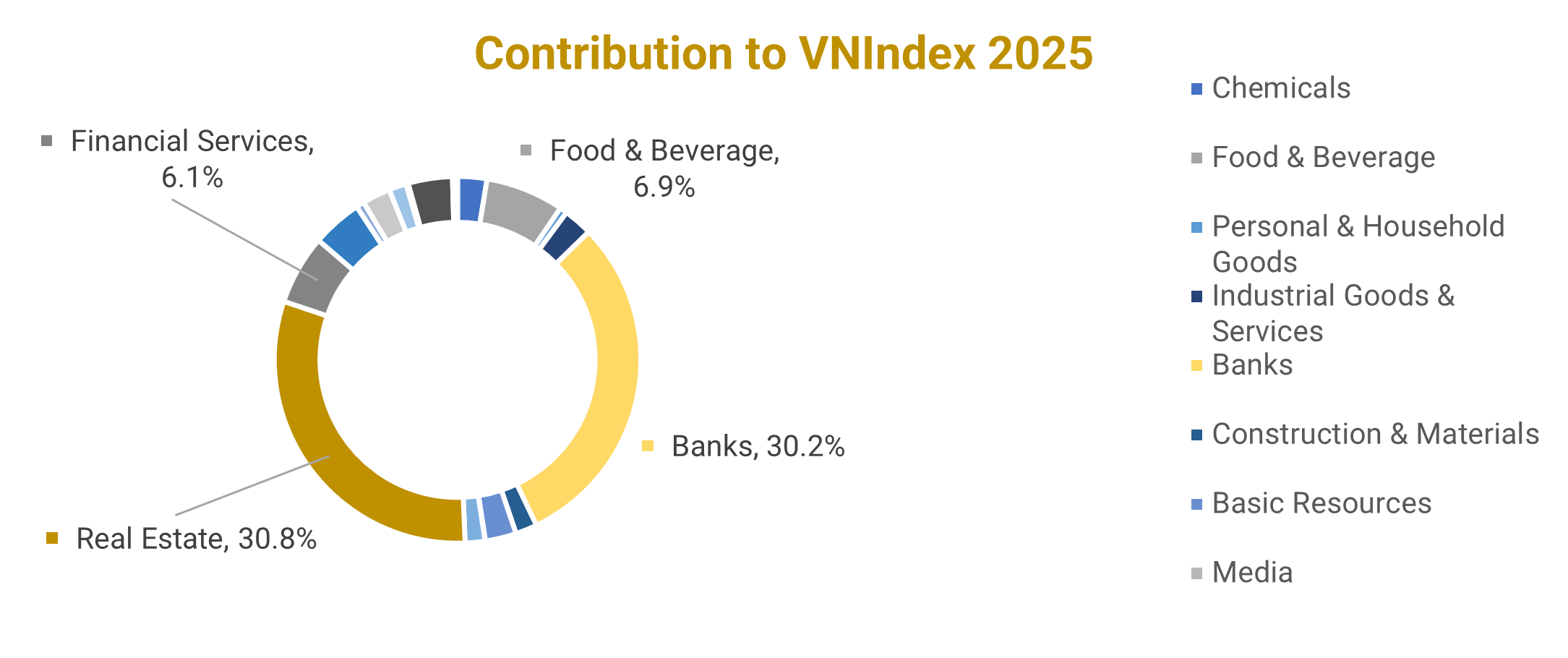

An inherent limitation is the structural imbalance of the Vietnamese stock market, which is heavily dominated by the banking and real estate sectors. As of the end of May 2026, these two industries accounted for 30.2% and 30.8% of HoSE’s total market capitalization, respectively. This highlights the complete absence of representatives from advanced tech industries such as AI or semiconductors, diminishing Vietnam’s attractiveness to global growth funds. Meanwhile, as the domestic real estate market cooled down under the impact of rising interest rates since late 2025, the growth momentum of these pillar stocks has been significantly impaired.

Source: FiinPro, PHFM Compiled

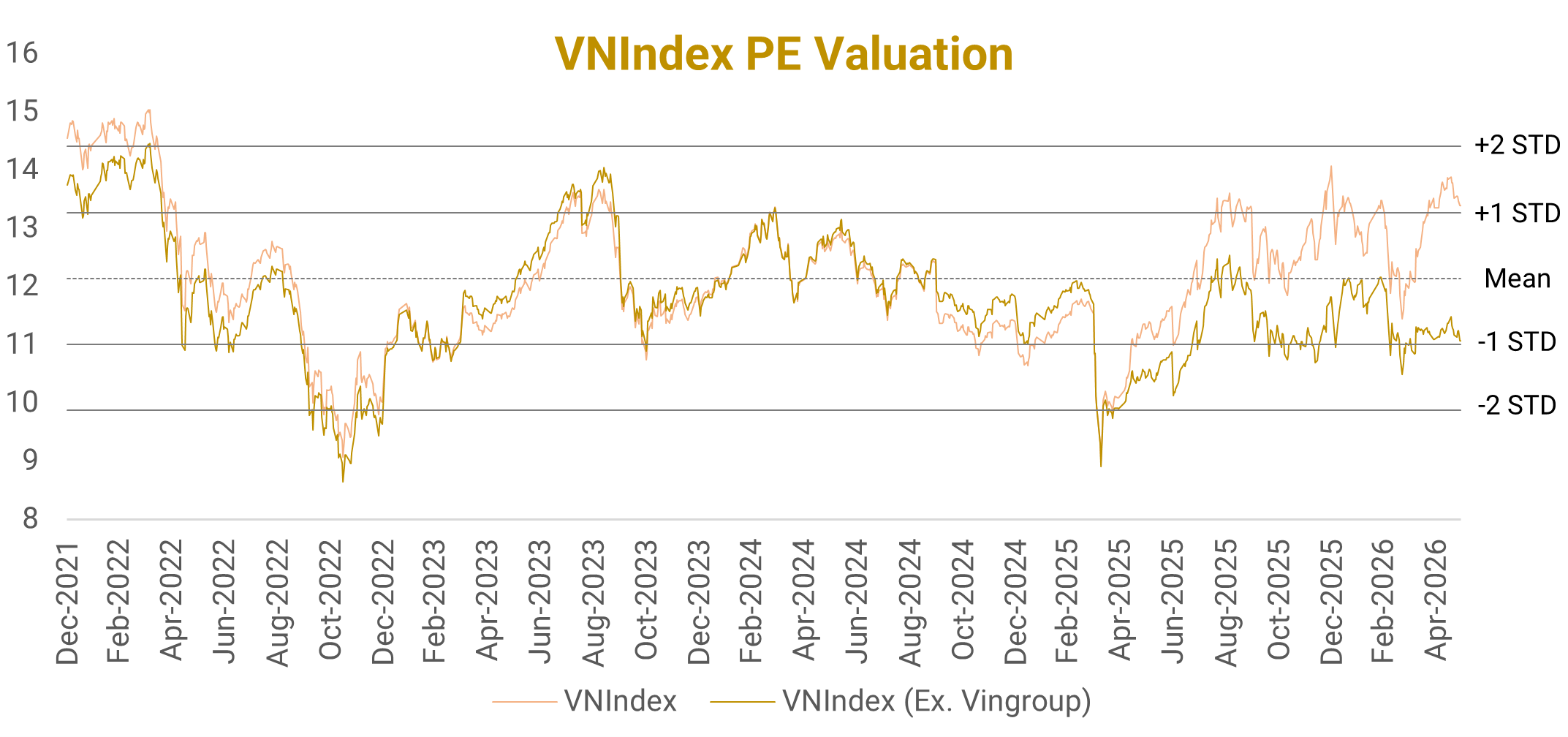

To clarify this point, let’s look at the valuation of the VN-Index compared to global markets recently. The P/E valuation for the VN-Index is only around 13.4x, and 10.1x if the Vingroup cluster is excluded (lower than the 5-year historical average). Despite a reasonable valuation, foreign capital continues to net withdraw from Vietnam.

Source: FiinPro, PHFM Compiled

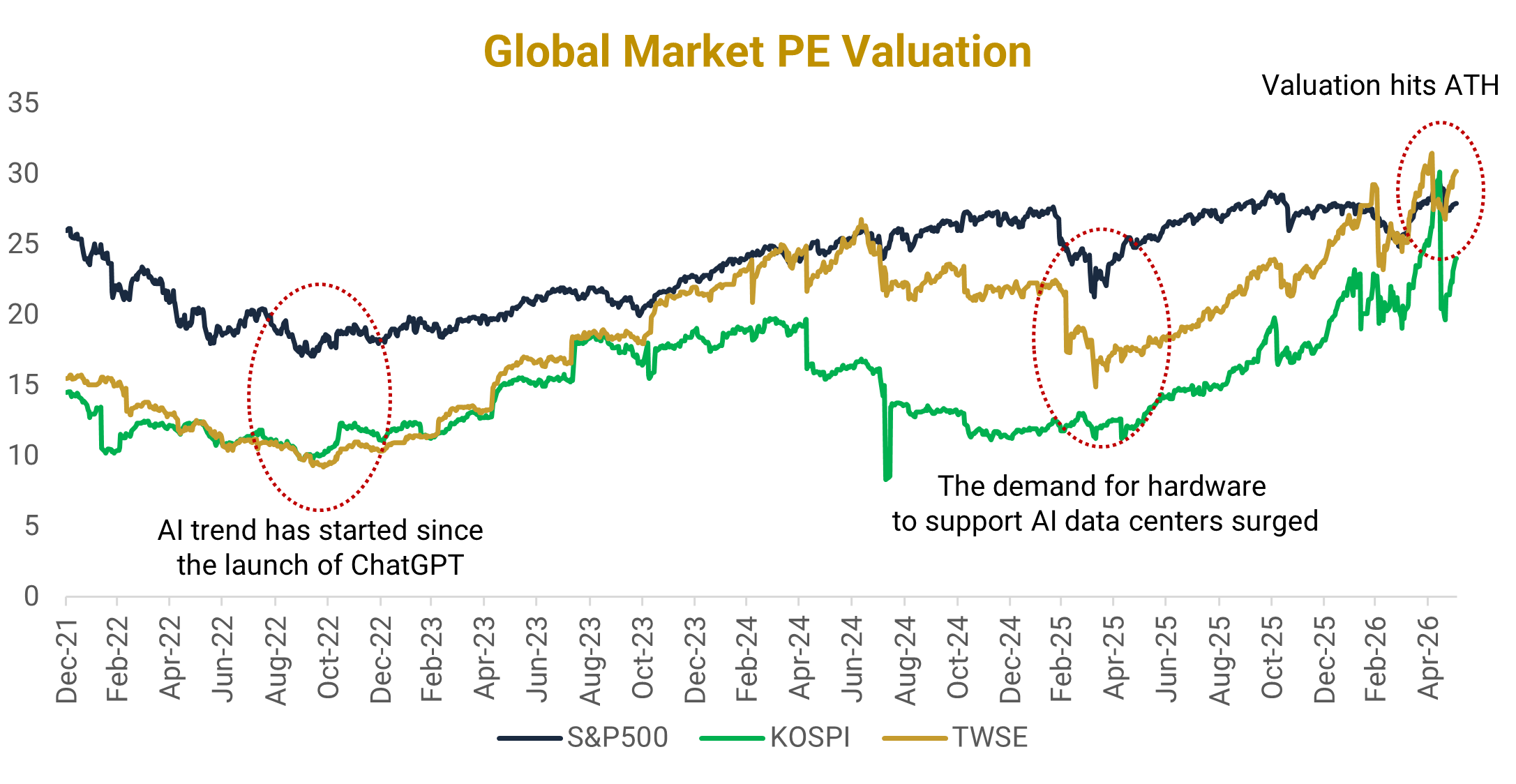

Conversely, cash flows are rotating into more promising markets, making them expensive. All three markets—the S&P 500, TWSE, and KOSPI—are currently being shaped by the next-generation industrial revolution: Artificial Intelligence (AI) and the global semiconductor supply chain.

– In Taiwan, TSMC accounts for more than 40% of the entire market capitalization.

– In South Korea, the KOSPI is spearheaded by Samsung Electronics and SK Hynix.

– In the US, the “Magnificent Seven” tech giants represent over 34% of the total capitalization of the S&P 500.

Source: Bloomberg, PHFM Compiled

3. MSCI Standards: Vietnam’s Next Station

To be excluded as a vulnerable frontier asset in term of global headwinds, Vietnam’s next destination is a market upgrade under MSCI criteria—the most prestigious benchmark that aggregates over 80% of global emerging-market-oriented capital.

Currently, Vietnam has only met 10 out of MSCI’s 18 market accessibility criteria. To be included in this organization’s upgrade watch list for the 2028–2029 period, Vietnam is strictly required to resolve the following three technical bottlenecks:

1. Foreign Ownership Limits (FOL): MSCI imposes stringent requirements on stock accessibility. Sensitive sectors remain under strict foreign room restrictions ranging from 0% to 51%, preventing large-scale funds from acquiring block shares. The implementation of solutions such as Non-Voting Depositary Receipts (NVDR) is an absolute necessity.

2. Foreign Exchange Market Liberalization: Administrative procedures regarding currency conversion and indirect capital transactions must be streamlined to the maximum extent to ensure that cash flows can move in and out seamlessly within the settlement day.

3. Independent Central Counterparty (CCP) Entity: While FTSE accepts the Non-Pre-Funding (NPF) solution under Circular No. 68/2024/TT-BTC as a stepping stone, MSCI requires the actual existence and safe operation of an independent CCP organization to guarantee settlement risks for all market participants. Bringing the CCP into operation from the beginning of 2027 will be the decisive milestone for Vietnam’s capability to achieve an MSCI upgrade.

4. Key Factors to Monitor to Attract Foreign Capital Flows

To optimize foreign capital inflows and minimize market volatility during the transition phase from September 2026 to September 2027, investors need to closely monitor the following factors:

– Diversifying the structure of listed commodities: Accelerate the equitization and listing process of large-scale State-Owned Enterprises (SOEs), while researching the application of Non-Voting Depositary Receipts (NVDR) to untie the foreign ownership limit knot while firmly preserving state control over key strategic sectors.

– Developing the domestic institutional investor base: Encourage the formation of domestic pension funds, insurance funds, and mutual funds to lessen the market’s reliance on short-term speculative cash flows from retail investors, establishing a more stable and sustainable valuation foundation.

Vo Hoang Long – Invesment Department, PHFM