INFLATION RETURNS, POLICY DIVERGES – NAVIGATING THE ROAD AHEAD

1. When Inflation Roars Back: A New Global Shock

The global macroeconomic environment in the first quarter of 2026 is defined by a severe resurgence of cost-push inflationary pressures, fundamentally altering the trajectory of central bank monetary policy. Throughout late 2025, markets operated with a projection of a stable global growth rate of 3.1% and inflation of 4.4% for the year. However, a significant geopolitical shock in the Middle East has rendered these assumptions obsolete, triggering a synchronized spike in global energy, logistics, and commodity costs.

The underlying tension across global markets is the delicate balancing act between containing this renewed inflation and sustaining economic growth. The conflict and subsequent blockade of the Strait of Hormuz—a vital maritime chokepoint handling approximately 35% of global seaborne crude oil trade and 20% of liquefied natural gas (LNG) exports—have triggered the largest initial disruption in global oil supply on record, removing roughly 10 million barrels per day from the market.

Consequently, Brent crude oil prices are forecasted to average $86 per barrel in 2026, a 24% surge from the previous year, while Asian LNG spot prices increased by over 140%. This energy shock operates as the first wave of a multi-stage inflationary pattern. The second wave is already materializing in agricultural and industrial inputs, with fertilizer prices projected to rise by 31%, heavily impacting future food prices. Finally, these elevated input costs are permeating wage and production structures, creating a formidable second-order core inflation impulse that Central Banks are now forced to confront.

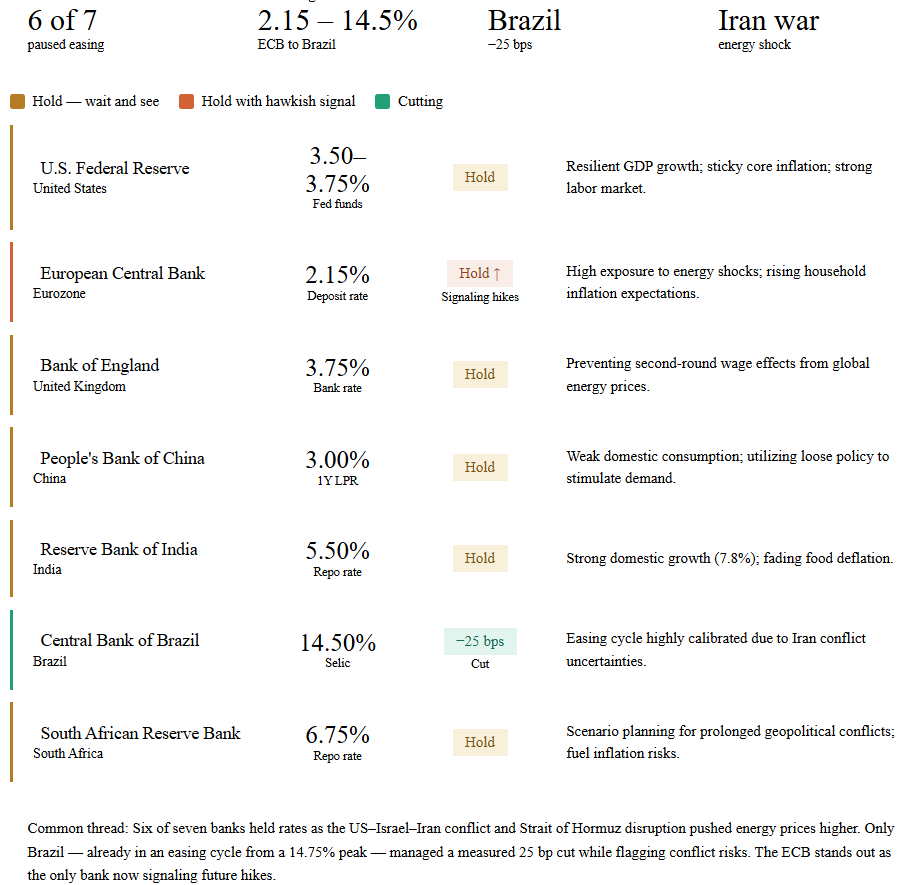

2. Central Banks on Alert: The End of Easy Money

The resurgence of energy-driven inflation has effectively ended the expectations for monetary easing in 2026. Central banks are displaying a stark divergence in their policy responses, influenced by their respective domestic economic resilience and exposure to global supply shocks.

3. Tightening or Holding: A Decisive Shift in Advanced Economies

In the United States, economic activity reflected a stable yet cautious expansion, with Q1 GDP growth estimated near 2.0% to 2.5%. This growth is heavily supported by high-income consumer spending and business investment. However, inflation data disrupted market optimism. Headline CPI accelerated to 3.3% year-over-year in March, while the core Personal Consumption Expenditures (PCE) rose by 3.0%. Survey data from financial officers indicates that corporate price growth expectations remain elevated at 3.6%. Consequently, the Federal Reserve paused its easing cycle, maintaining the federal funds rate at 3.50% to 3.75%, with markets pricing in a prolonged holding pattern.

The European Central Bank (ECB) has signaled one of the most pronounced hawkish shifts among major institutions. The Eurozone remains structurally vulnerable to global energy prices, warning an escalation in inflation risks. Fuel prices could permeate the European economy faster than during the 2021-2022 crisis, prompting preemptive price hikes even amidst subdued demand. Financial markets have reacted by pricing in three to four ECB rate hikes over the next twelve months, potentially lifting the key deposit rate to a range of 2.75% to 3.0%, beginning as early as June 2026.

Similarly, the Bank of England (BoE) maintained the Bank Rate at 3.75% in April 2026. With UK CPI inflation printing at 3.3% in March, the BoE explicitly noted that while monetary policy cannot directly influence global energy prices, it must act aggressively to lean against material second-round effects in domestic price and wage-setting.

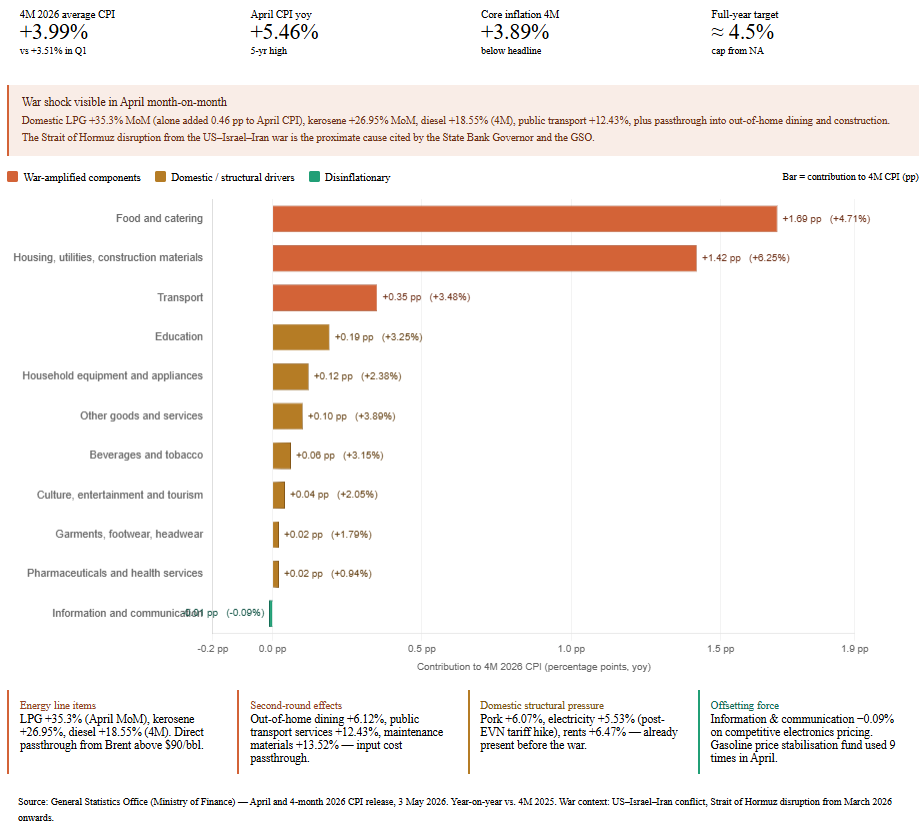

4. Vietnam in the Same Current: Domestic Pressures Mount

Vietnam presents a critical case study of an emerging market successfully navigating severe imported inflation while aggressively pursuing domestic economic expansion. In the first quarter of 2026, the Vietnamese economy expanded by an estimated 7.83% year-over-year, driven by robust industrial production and a 9.1% surge in foreign direct investment (FDI) disbursements, which reached $5.4 billion.

Despite this growth, the domestic economy is facing acute cost-push inflation. The Consumer Price Index (CPI) climbed to 5.46% year-over-year in April 2026, accelerating sharply from 4.65% in March, while core inflation remained elevated at 4.66%.

The primary drivers of this inflationary spike are heavily concentrated in externally influenced sectors. Transportation costs surged by 11.1% in April due to the global crude oil shock, while the food category increased by 5.2%. Together, these categories account for more than half of the Vietnamese CPI basket. Furthermore, the government is managing scheduled domestic adjustments, including an 8.9% projected increase in healthcare services driven by rising management costs and medical staff allowances.

To counter these pressures, the Ministry of Finance has intensified a dual approach: tightening administrative price controls while accelerating public investment disbursement to sustain the national 10% GDP growth ambition. Monetarily, the State Bank of Vietnam (SBV) has maintained a highly accommodative stance to shield the domestic economy. The benchmark interest rate remains unchanged at 4.50%, with a system-wide credit growth target set at 15% for the year.

5. Upcoming Trend: Be Cautious Amid Global Instability

Global inflation is projected to remain elevated, impacting on consumer trends and monetary policy. The current inflationary pressure operates in multiple waves—starting with immediate energy shocks and subsequently feeding into food and core services—the era of central bank rate cuts has been officially delayed.

Investors should anticipate a “higher-for-longer” interest rate environment globally. The U.S. Federal Reserve and the Bank of England are expected to maintain their current rates to assess incoming data and prevent second-round wage effects. Conversely, regions highly exposed to energy imports, such as the Eurozone, may actively hike rates to prevent long-term inflation expectations from spiraling.

6. Strategic Asset Allocation: Hedging Against Sticky Inflation and Volatility

In a higher-for-longer monetary regime, capital preservation and inflation protection are paramount.

🔸 Fixed Income: Investors should consider minimizing duration risk. Short-term 3-6M Certificate Deposit or Term Deposit are strategic vehicles for protecting purchasing power while capturing yield. Bond funds, especially medium- and long-term bond funds, are not the optimal choice at this time. Investing in corporate bonds carries a higher risk of default as inflation and high capital costs negatively impact company profit margins and weaken market purchasing power. Weakened operating cash flow, coupled with soaring debt refinancing costs, increases the default risk for issuers to alarming levels.

🔸 Targeted Equities: Despite domestic inflationary headwinds, the country’s ambitious 10% GDP growth target, robust infrastructure investment, and the structural catalyst of a potential FTSE Emerging Market upgrade in late 2026 provide a compelling case for targeted equity exposure. Investors should shift from diversified approach to a selective approach, prioritizing companies with defensive characteristics and strong fundamentals.

🔸 Some key characteristics to consider during this period include:

(i) Cash-Rich Stocks: Companies with significantly higher cash and cash equivalents than debt, less reliance on credit, and the ability to generate financial income in a high-interest-rate environment.

(ii) High-and-Stable Dividend Yield Stock: Suitable for investors seeking sustainable passive income.

(iii) Leading Stocks with Attractive Valuation.

Vo Hoang Long – Investment Department, PHFM