THE POWER SECTOR IS ENTERING A NEW INVESTMENT CYCLE

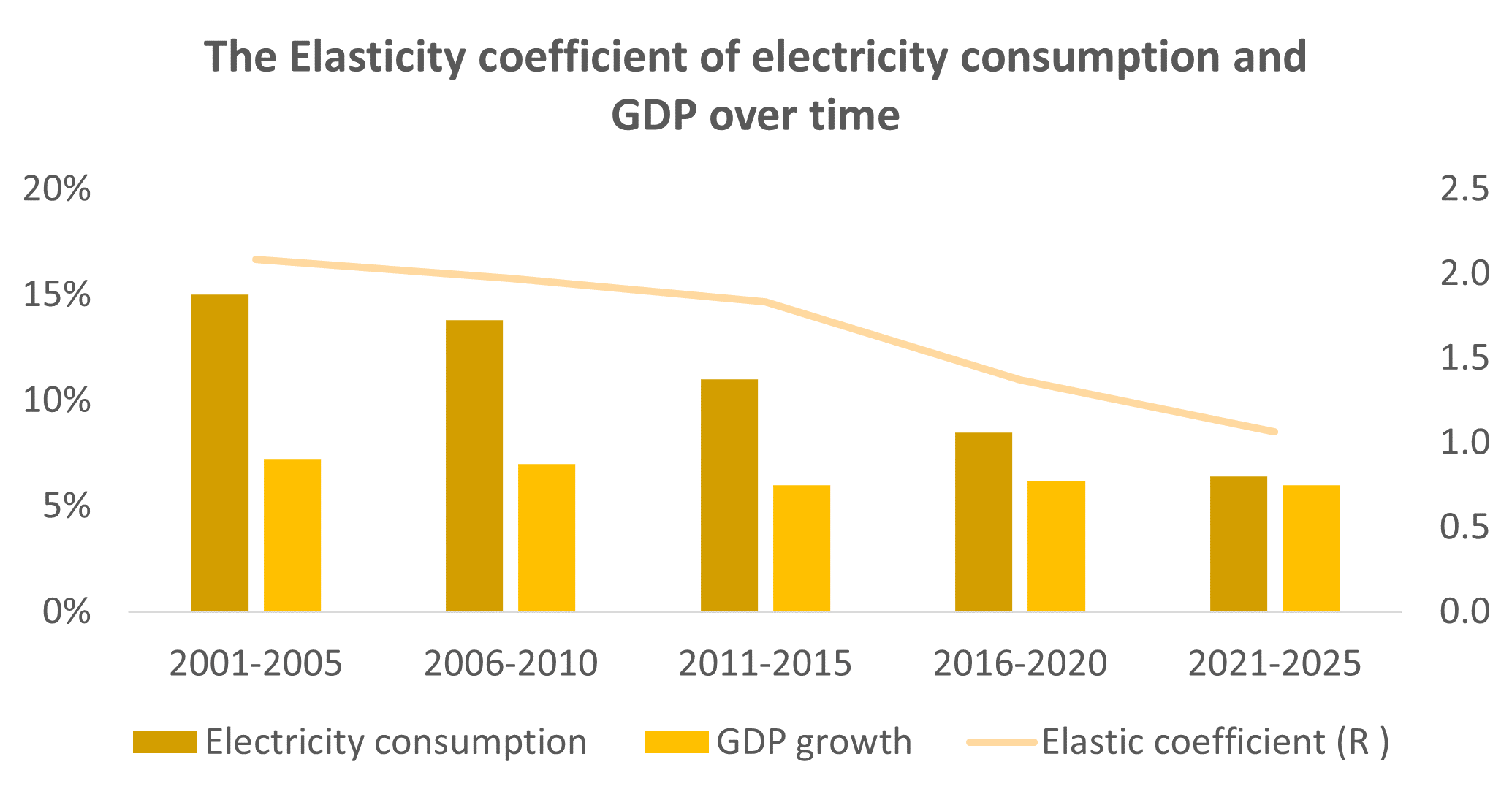

Electricity consumption growth remains high

Electricity demand in Vietnam continues to grow, but the pace of that growth has slowed relative to the pace of economic expansion. This is captured by the “Electricity Elasticity Coefficient with respect to GDP”, which represents the relationship between the growth rate of electricity demand (E) and the growth rate of GDP (ΔE%/ΔGDP%). In Vietnam, the ratio was around 2 during 2000-2010, meaning electricity demand grew twice as fast as GDP. It then declined to 1.8 in 2011-2015, and further to 1.4 from 2016-2020. Notably, in 2021-2025, the elasticity coefficient was only 1.1, a period that also witnessed the consequences of the COVID-19 pandemic. The clear trend is that the electricity/GDP elasticity coefficient is decreasing, a trend observed in other countries worldwide where, as the economy develops, this index tends to fall below 1.

(Source: EVN, PHFM)

In Vietnam, the industrial sector drives energy consumption growth, accounting for nearly 55% of electricity consumption, the highest among all sectors. However, its growth rate has slowed down over the past five years compared to other sectors. Residential consumption accounts for approximately 35% of total output, while trade, services, and restaurants account for over 7%. Electricity for the agricultural sector accounts for only a small percentage, about 3%. We believe that Vietnam’s electricity consumption will continue to grow at a high rate as the country focuses on developing more energy-intensive industries such as metallurgy, mechanical engineering, and data centers to complete the domestic product supply chain.

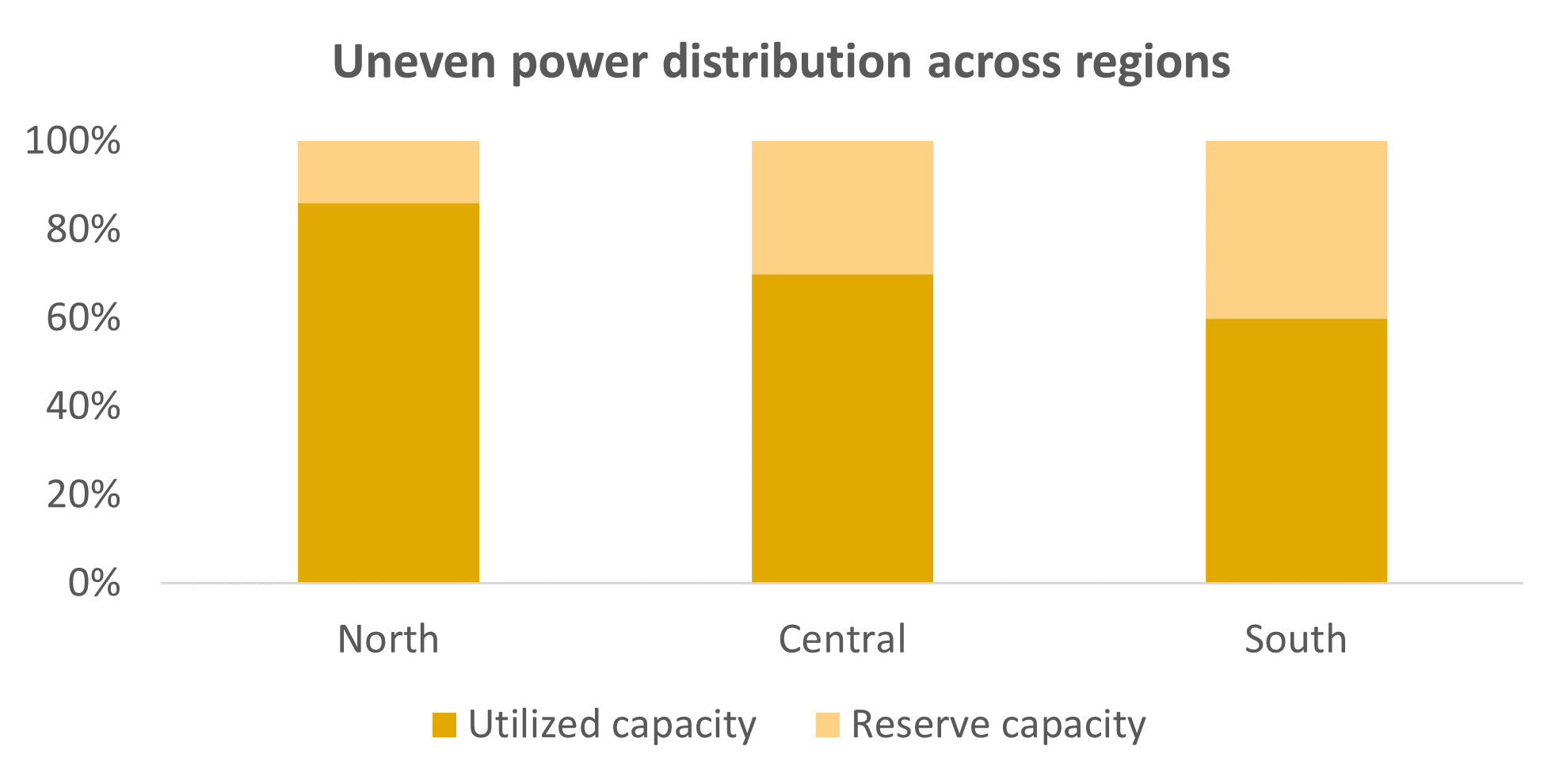

Regional imbalance

Regional imbalances in electricity supply and demand, especially the severe shortage risk in the North, are putting heavy strain on the national transmission system as large amounts of power are transported from the Central and Southern regions to the North.

The Northern region faces the risk of electricity shortages, with reserve capacity reaching only about 14%, compared to 70% in the Central region and 40% in the Southern region. This is due to the strong increase in consumption demand in the 2021-2025 period (CAGR +12%/year) higher than the national average, while electricity supply is stagnant due to:

(1) In the 2019-2021 period, the total industry capacity increased sharply thanks to the issuance of FiT (Feed-in Tariff) prices for renewable energy projects, but renewable energy development in the North is limited compared to the Central & Southern regions – where the climate is more favorable.

(2) In the 2021-2025 period, capacity increase is slow, mostly from transitional projects (including projects that are behind schedule and have not yet been put into commercial operation (COD) within the FiT period). Furthermore, new projects have also had to be temporarily suspended due to the lack of a legal basis for signing power purchase agreements (PPAs) with EVN, as the Ministry of Industry and Trade has been slow to issue a new pricing framework.

(Source: EVN, PHFM)

The power transmission system is under significant pressure due to the increased transmission of electricity from the Central and Southern regions to the North, stemming from the imbalance between electricity supply and demand between these regions. To ensure energy security, investment in the 500kV inter-regional transmission grid infrastructure has been accelerated, achieving a CAGR of +9.0% per year in 2021-2025. However, new investments have only reached nearly 70% of the target set for the 2021-2025 period, according to the Power Development Plan VIII, failing to keep pace with the actual load growth rate in the North (CAGR of +12.0% per year). This is due to difficulties in securing funding for EVN, causing delays in the implementation of transmission projects compared to the plan.

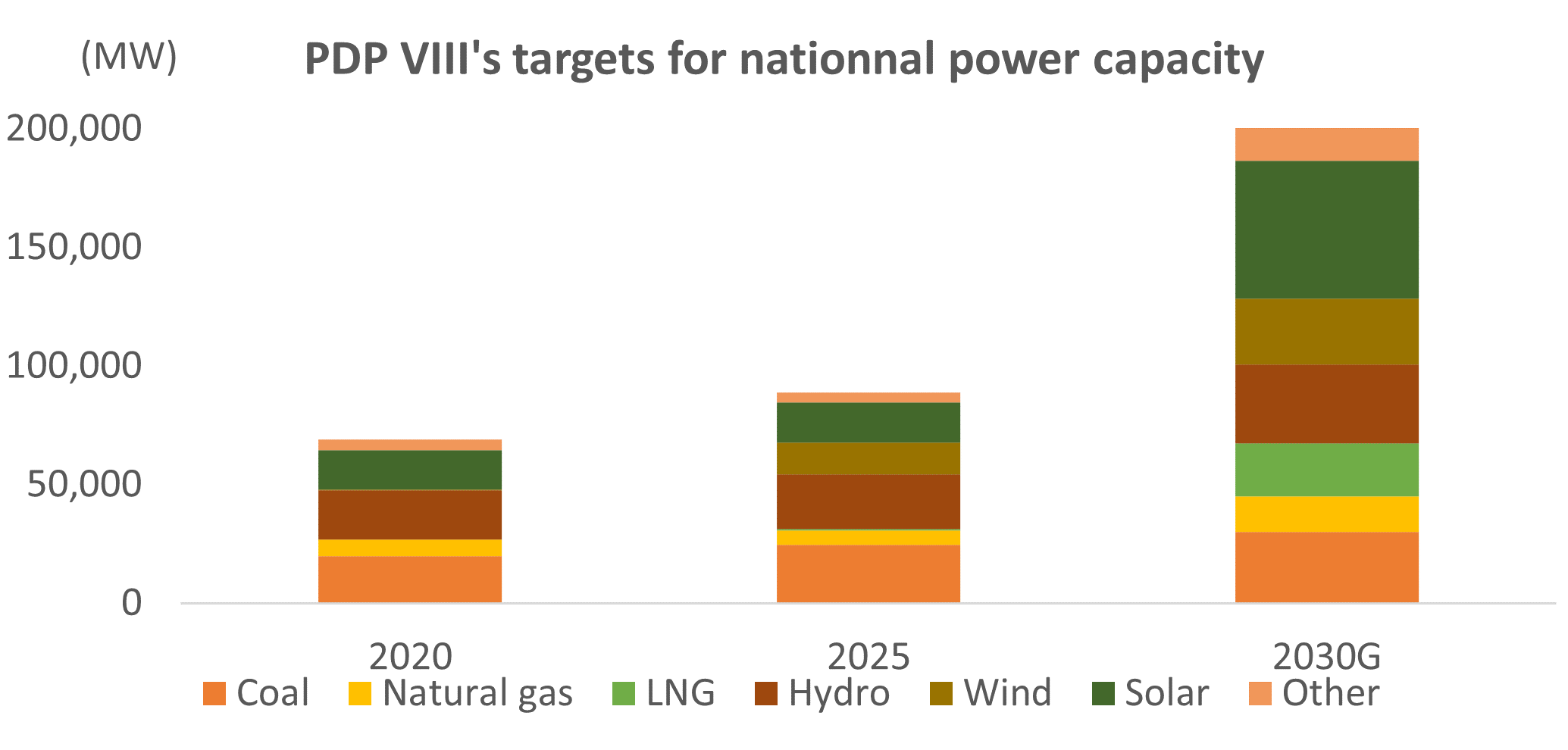

The ambitious revised Power Development Plan VIII

The ambitious revised Power Development Plan VIII opens the door for renewed private investment after a prolonged policy gap, aiming to provide enough supply to support 10% annual GDP growth in 2026-2030.

Vietnam has raised its economic growth target to 10% per year for 2026-2030, which will drive sharply higher electricity demand. To meet this goal, the government is gradually reopening investment in the electricity sector with four main policy focuses: issuing a new pricing framework to attract private developers back into power generation; finalizing the legal framework for the direct power purchase agreement (DPPA) mechanism and two-component pricing; removing legal obstacles from previous projects to restore investor confidence; and allowing private participation in transmission infrastructure to reduce the capital burden on EVN and accelerate the upgrading of the national power grid; promote the implementation progress of the Revised Power Plan VIII by resolving bottlenecks that have slowed down the plan’s implementation in the past.

(Source: EVN, PHFM)

According to the revised plan, total electricity production and imports are projected to reach 560-624 billion kWh by 2030, more than double the 2025 level, to support the targeted growth (10% annual GDP growth in 2026-2030). Total installed capacity is expected to reach 183-236 GW by 2030, an increase of 100-168% compared to 2025 and 50 GW higher than the previous plan, driven mainly by solar, wind, and LNG. The plan also prioritizes major transmission expansions to reduce pressure on the 500 kV North-South line, alleviate excess renewable capacity in the South Central and Southern regions, and ensure reliable supply in the North, which is prone to shortages. The outlook for investment in transmission infrastructure is strengthened by EVN’s improved ability to secure funding for transmission system investments in the 2025-2030 period, following the government’s approval of adjustments to retail electricity prices. It is estimated that Vietnam needs planned and directed capital of up to US$136 billion to develop power sources in the 2026-2030 period.

LNG power is one of the main growth drivers in the next 5 years

The 8th National Power Development Plan (QHĐ8) aims for a strong expansion of gas-fired power capacity. Domestic gas-fired power capacity is expected to increase from 7 GW to 15 GW by 2030, mainly thanks to the gas source from the Block B project, while LNG gas-fired power capacity is targeted to increase to 23 GW. However, by the end of 2025, only two LNG gas-fired power projects, Nhon Trach 3 & 4, have been put into operation, while most other projects, such as O Mon 4, are still in their early stages. This delay poses risks to the overall goals of the 8th National Power Development Plan. As coal-fired power is expected to be phased out after 2030 and hydropower no longer has room for development, Vietnam’s future electricity supply will have to rely on renewable energy and gas-fired power plants. However, renewable energy sources such as solar and wind power are intermittent and require other power sources to run in the background. Therefore, gas-fired power plays a vital role in providing flexible base capacity to supplement renewable energy.

(Source: EVN, PHFM)

In conclusion, Vietnam’s electricity sector is entering a period of rapid growth with three main structural trends: accelerating the development of LNG-fired thermal power plants to fill the gap in renewable energy, expanding the transmission network to reduce power curtailment rates and free up inter-regional electricity, and developing offshore wind power in the long term. The listed power companies, as well as the electricity sector in general, will have the opportunity to benefit from these trends by leveraging their strengths in LNG project implementation, EPC general contracting, operating gas-fired thermal power plants, and a renewable energy platform ready for the DPPA mechanism.

Phung Minh Hoang – Investment Department, PHFM